|

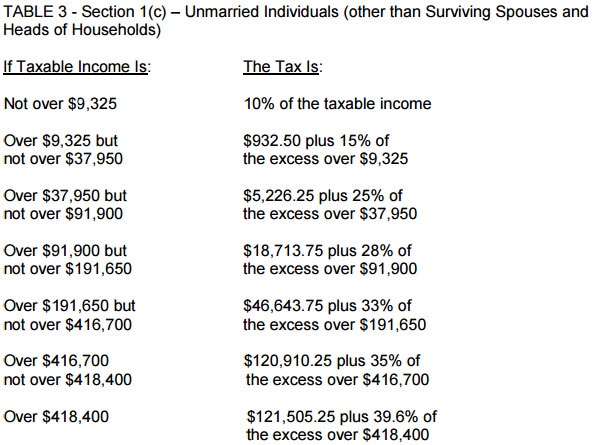

The great recession and ongoing recovery hasn't been very good to retirees living on a fixed income and savers who put money in a savings account. Bank yields have been pretty low and supposedly that is going to change with the improving economy and rising interest rates. People have had to go invest to other investments to maintain a decent standard of living. Other alternatives options include buying real estate, investing in the stock market, investing in your business, art, precious metals, and other items that can appreciate. California Tax Free bonds are a good investment to put a portion of your nest egg if you live in this high tax state to reduce your tax liability. It's a good balance against the high stock market (currently the Dow's at 19,780) on 1/18/2017. For example, as a single individual in 2017,  Directly from the IRS website at https://www.irs.gov/pub/irs-drop/rp-16-55.pdf Additionally, living in the state of California, means that any income from $51,531 to $262,222 is taxed at 9.3%.

Anyone who is making above $191,650 should definitely look into CA Tax Free Funds. Any income you make over that is effectively taxed at 42.3%. CA Tax Free Bond Funds allow you to not pay any federal or state tax on the income generated by these financial instruments. Currently, many top rated CA mutual funds are returning over 4% and one would need to find an taxable equivalent investment yielding over 6.9% at this income level to be comparable. There's an expense fee associated with these funds that could be as high as .9 or as low as .2. Vanguard is usually the lowest and you could get fees down to 0.12% with their Admiral Shares.

0 Comments

If you work for a company that has a 401(k) plan, you should be saving for retirement unless you A. expect to hit the lottery in the future, B. are a trust fund baby, or C. would enjoy growing old and being homeless. If neither of the three apply to you, please continue reading! First off, you should hopefully be spending less than what you make. Second, if you have any debt, you should be paying off the highest interest rate debt off first. Then you should try and have an emergency savings in case you lose your job. Only, then should you think about retirement savings. And remember, the earlier you start, the faster money can grow due to compound interest. Assuming that you'd be able to start and save for retirement today, you should always contribute what your company matches at the very least. For example, if I contribute 2% of my salary to my 401(k), my company will match 2% of my pay. When I contribute up to 5% of my salary to my 401(k), my company will match up to 4% of my pay. Anything above that, my company will only match 4%. If you don't contribute to the maximum of what your company will match, you might as well start burning up dollar bills. Next you may have the choice of placing savings into a regular 401(k) or a Roth 401(k). Pre-tax money you put into a regular 401(k) is taxed later when you take it out upon retirement. You should put money into a 401(k) if you expect to be in a lower tax bracket when you retire and/or think that U.S. tax rates will be lower when you retire. Otherwise, a Roth 401(k) is what you should choose if you think that you will be in a higher tax bracket when you retire and think that U.S. tax rates will be higher when you retire. The maximum you can contribute is $18,000 as of this year (2016), so if you can max that out, your future self will thank you. I personally use low-cost index funds like Vanguard.  If you're very healthy, have minimal medical bills, and if your company health plan offers it, you can also utilize your Health Savings Account (HSA) as a stealth retirement savings account. These high deductible health plans have a contribution limit of $3,350 this year. These contributions are tax deductible, savings can grow tax free, and savings are always available for qualified medical expenses year after year. Some plans also allow you to invest in stocks and bonds after hitting a certain savings limit. Make sure that this is for you, because if you do have health issues, the money spent on your high deductible plan yearly might not be worth it in the long run.

Before age 65, you can always withdrawal these funds for qualified medical expenses and not incur any penalties. But, after age 65, you can withdrawal this money and use it for any non-medical expenses but you will be taxed similarly like a regular 401(k). Also, if your company is public and participates in a stock purchase plan, be sure to take part in it, especially if you are able to purchase stock at a discounted price! Regardless of your company's future, if you are able to buy the stock at a discounted rate and can sell it at the open market immediately at a higher price, that's money. Otherwise, feel free to invest in your company as much as you feel comfortable. Just remember that working at a company with the majority of your net worth in company stock can be risky. Ex-Enron employees are a perfect example. Other than that, be sure to exercise, eat healthy, and brush/floss your teeth. Be sure to utilize your health plans for all the preventative care that you are eligible for! |

Photos used under Creative Commons from complexsearch, quinn.anya, foundin_a_attic, Mike Licht, NotionsCapital.com, Carlos ZGZ, www.hickey-fry.com, Andrew Stawarz, dejankrsmanovic, Maria Eklind, [SiK-photo], Porto Bay Trade, Stefans02, Alan Light, investmentzen, Prayitno / Thank you for (11 millions +) views, mcortez121, supportcaringllc